Understanding the bankruptcy process is crucial when evaluating if it’s the right choice for your situation. This guide covers key factors to consider when filing bankruptcy.

1. Qualifying for Bankruptcy

-

- Financial Distress: Individuals typically qualify if unable to pay debts and facing hardship like wage garnishment or foreclosure.

- Means Testing: Applies to Chapter 7; compares income to state median; high earners may be required to file Chapter 13 instead.

- Credit Counseling: Must receive credit counseling 180 days before filing; proves bankruptcy as last resort.

- Previous Filings: Restrictions exist on how often you can file; varies by chapter.

Example: Dan’s Bankruptcy Qualification

-

- Dan lost his job and was unable to pay his debts.

- He qualified for Chapter 7 based on means testing.

- Completed credit counseling 6 months prior.

Tips on Qualifying for Bankruptcy

-

- Consult a bankruptcy attorney to assess eligibility.

- Calculate income and expenses to determine financial state.

- Research filing restrictions based on previous bankruptcy cases.

Frequently Asked Questions

-

- What are common signs someone may qualify for bankruptcy? Struggling to pay bills, creditor harassment, wage garnishment, home foreclosure threat.

- Do income limits apply for Chapter 7 bankruptcy? Yes, means testing compares income to state median; higher earners file Chapter 13.

- How soon after credit counseling can you file bankruptcy? Bankruptcy filing must be at least 180 days after counseling session.

2. Chapters of Bankruptcy

-

- Chapter 7: Liquidation; eligible assets sold to pay creditors; remaining debts discharged.

- Chapter 13: Debt reorganization; debtor keeps assets; repays creditors through payment plan.

- Chapter 11: Business reorganization; company remains operating while repaying creditors.

Example: Comparing Bankruptcy Chapters

-

- Chapter 7 – Assets liquidated, remaining debts discharged.

- Chapter 13 – Debts reorganized and repaid through payment plan.

- Chapter 11 – Business remains operating while repaying creditors.

Tips on Choosing the Right Chapter

-

- Evaluate assets at risk for liquidation under Chapter 7.

- Assess income stability to determine feasibility of Chapter 13 plan.

- Chapter 11 makes sense if aiming to reorganize and save a business.

Frequently Asked Questions

-

- Can you choose which bankruptcy chapter to file under? Yes, but you must meet eligibility criteria for the specific chapter.

- Do you keep property when filing Chapter 7? Some property is exempt; anything non-exempt may be liquidated.

- How long does the bankruptcy stay on your credit report? Chapter 13 remains for 7 years; Chapter 7 remains for 10 years.

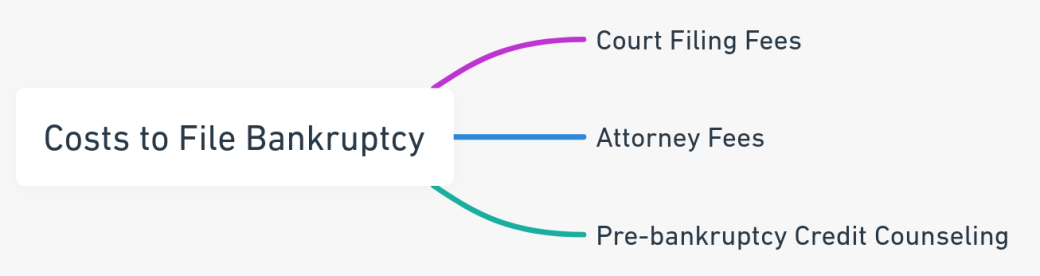

3. Costs to File

-

- Court Filing Fees: Vary by chapter choice; due when petition is filed; Chapter 7 fee is $338.

- Attorney Fees: Average $1,500-$3,000 for less complex filings; higher for complex cases; paid up front or via payment plan.

- Pre-bankruptcy Credit Counseling: Required counseling averages $50-$100 and paid directly to agency.

Example of Bankruptcy Costs

-

- $338 court filing fee for Chapter 7

- $2,500 attorney fees, paid over 12 months

- $75 for pre-filing credit counseling session

Tips on Managing Bankruptcy Costs

-

- Research average attorney fees to set realistic budget.

- Ask about payment plans if unable to pay attorney fee upfront.

- Compare credit counseling agencies for most affordable option.

Frequently Asked Questions

-

- Can you file bankruptcy without an attorney? Possible but not recommended; attorneys navigate process.

- Are there payment plans for attorney fees? Yes, many lawyers offer affordable monthly payment options.

- Can the court filing fee be waived for financial hardship? Yes, you can request a filing fee waiver from the court.

4. Meeting of Creditors

-

- Attendance Required: Debtor must attend; failure to appear can lead to case dismissal.

- Under Oath: Debtor is placed under oath and answers questions about financial affairs.

- Creditor Participation: Creditors can attend and ask questions if desired.

Example Meeting of Creditors Experience

-

- Debtor attended and provided testimony under oath.

- Trustee asked questions about income, assets, debts.

- Few creditors attended or participated.

Tips for the Meeting of Creditors

-

- Review case with attorney to prepare for potential questions.

- Bring required documents like tax returns and pay stubs.

- Listen to trustee carefully and answer questions accurately.

Frequently Asked Questions

-

- Where are meetings of creditors held? Typically at courthouses, federal buildings, or trustee offices.

- What happens if you miss the meeting of creditors? The court may dismiss your bankruptcy case if you fail to appear at the required meeting.

- Can you reschedule the meeting of creditors? Yes, if you have a valid conflict, your attorney can request to reschedule the meeting.

5. Timeline of the Process

-

- Petition Filing: Case formally begins when bankruptcy petition is filed with court.

- Automatic Stay: Collection against debts is halted upon filing; creditors must cease contact.

- Meeting of Creditors: Held about 30-60 days after filing; debtor questioned under oath.

- Discharge Granted: Court order releasing debtor from liability for dischargeable debts; timing varies.

Example Bankruptcy Timeline

-

- Filed Chapter 7 petition on 1/5/2023

- Automatic stay halted collection immediately

- Meeting of creditors held on 2/15/2023

- Discharge granted on 5/20/2023

Tips on Navigating the Timeline

-

- Stay organized with deadlines for required documents and financial records.

- Notify creditors of automatic stay to halt collections immediately.

- Don’t miss the meeting of creditors or discharge may be denied.

Frequently Asked Questions

-

- How soon after filing is the automatic stay effective? Immediately upon petition filing.

- When does discharge relieve debts? After all required documents submitted and no objections from creditors.

- How long does the bankruptcy process take? Typically 3-6 months until discharge granted.

6. Debts Discharged

-

- Elimination of Debt: Discharge provides fresh start by eliminating legal obligation to pay.

- Exceptions Apply: Certain debts like taxes, fines, alimony cannot be discharged.

- Ongoing Liens: Discharge removes personal liability but valid liens remain on property.

Example of Discharged Debts

-

- Credit card balances eliminated

- Medical debts removed

- Mortgage lien remains on property

Tips on Understanding Debt Discharge

-

- Review non-dischargeable debts to avoid surprises.

- Consult attorney on validity of any liens remaining after discharge.

- Keep making payments on reaffirmed debt until paid off.

Frequently Asked Questions

-

- What types of debts are not discharged in bankruptcy? Taxes, student loans, child support, alimony, court fines.

- Is a mortgage eliminated with Chapter 7 bankruptcy? No, the underlying lien remains even when personal liability is discharged.

- Can you voluntarily repay a discharged debt? Yes, you can voluntarily repay debts for moral reasons.

7. Rebuilding Credit After Bankruptcy

-

- Negative Impact: Bankruptcy damages credit score, especially right after filing.

- Gradual Rebound: Credit score typically rebounds and improves over time.

- Disciplined Habits: On-time payments, low balances, and financial prudence help demonstrate changed behavior.

Example Credit Rebuilding Journey

-

- Score dropped 100 points after filing

- Regained 50 points in 12 months of responsible habits

- Continues making payments on time and keeping balances low

Tips for Rebuilding Credit

-

- Get secured credit card and use responsibly to show positive payment activity.

- Avoid high balances and minimize credit inquiries.

- Check credit reports for errors and file disputes promptly.

Frequently Asked Questions

-

- How long does bankruptcy stay on your credit report? Up to 10 years from filing date.

- How soon can you get a credit card after bankruptcy? Usually within 6-12 months, often starting with secured cards.

- Does the impact of bankruptcy lessen over time? Yes, the negative effect on your credit score decreases as time passes.

Need Help With Bankruptcy Filing?

Contact us to speak with a knowledgeable bankruptcy attorney and if you need guidance on the process and to determine if filing is right for your situation.