This guide serves as a toolkit for evaluating critical formations – Limited Liability Companies (LLCs) vs. Corporations – empowering informed decisions tailored to your professional goals.

We outline key factors like owner liability, taxation frameworks, governance flexibility, startup costs and compliance protocols when weighing LLCs vs Corps to insure your venture gets off to the soundest legal footing.

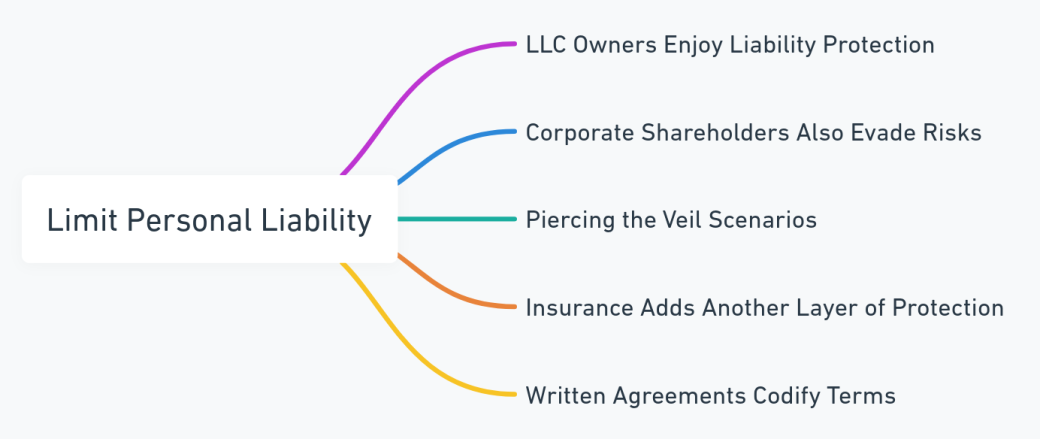

1. Limit Personal Liability

-

- LLC Owners Enjoy Liability Protection: Except in cases of fraud/misconduct, personal assets remain shielded.

- Corporate Shareholders Also Evade Risks: Directors & Officers may still have exposures.

- Piercing the Veil Scenarios: Courts may hold owners accountable for certain company debts.

- Insurance Adds Another Layer of Protection: Reduces exposures beyond entity structures.

- Written Agreements Codify Terms: Help strengthen limited personal liability arguments legally.

LLC Examples:

-

- James’ LLC construction business lawsuit did not endanger his personal home/assets when his company was sued.

- Paula included specific limited liability provisions in her LLC operating agreement reinforcing legal protections against individual member asset exposure.

- Kim’s LLC dissolution due to insolvency still left her personal car, retirement accounts and inherited properties untouched by creditors.

- Jada insured her LLC against professional errors and omissions liabilities to prevent any legal gray areas threatening her personal finances.

- The court ruled Mark’s oral promise to cover company obligations wasn’t enforceable to seize his bank account funds per the LLC structure.

- A supplier lawsuit against Alex’s single-member LLC left his personal vacation home fully protected as untouchable separate property.

Corporation Examples:

-

- Wendy’s personal finances stayed fully protected when her corporation faced a costly patent infringement lawsuit from a competitor.

- John proactively took out Directors & Officers liability insurance shielding his personal assets from any potential errors arising in his corporation.

- When Acme Corp folded due to insolvency, shareholders weren’t found personally responsible for unpaid company debts nor compelled to repay creditors from personal bankrupt.

- Banks dismissed allegations seeking to hold Henry accountable for his corporation’s loan defaults highlighting limited shareholder protections.

- Courts reinforced the separate legal identity between Salma’s corporation and herself as owner to prevent personal liability for lawsuits against her consulting business.

- Richard’s personal assets remained protected despite his video production company continually underpaying freelancers per independent contractor agreements.

How to Proceed:

-

- Analyze your full risk profile – evaluate where personal liability exposures might emerge before finalizing an entity choice.

- Inject caution language reinforcing limited liability protections into operating agreements/bylaws wherever possible.

- See if company general liability insurance policies cover owners too or purchase dedicated protection like D&O insurance.

- Solo entrepreneurs should maximize LLC usage for added insulation compared to Sole Proprietorships.

- Beware blurring personal-corporate finances, avoid undercapitalization jeopardizing veil protections.

- Upon dissolution, follow formal winding down procedures to contain enterprise liabilities from hitting owners.

FAQs:

-

- What paperwork formally establishes limited liability protections? Filing certificate/articles of organization registers entity creation and corresponding owner protections legally.

- How difficult is it for creditors to pierce the corporate veil outside fraud? Extremely challenging – courts recognize and reinforce liability shields for incorporated businesses.

- Can I be forced to sell personal assets to repay company obligations? No, remaining personal assets stay protected outside bankruptcy scenarios dissolving limited liability.

- What happens if LLC operating agreement lacks liability provisions? Default state laws governing LLCs still afford full liability limitations for members.

- Is it advisable to form single-owner LLCs over sole proprietorships? Strongly recommended for significantly better personal asset protection offered.

- Can erroneous personal guarantees on loans invalidate liability shields? Unfortunately yes, so review all documents cautiously shielding personal assets.

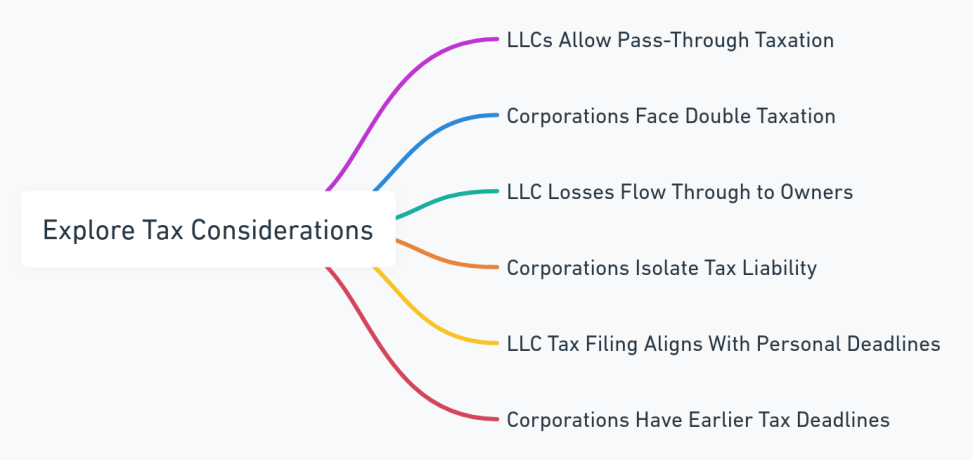

2. Explore Tax Considerations

-

- LLCs Allow Pass-Through Taxation: Income/losses passed to owners avoiding corporate double taxation.

- Corporations Face Double Taxation: Entity income taxed and shareholder dividends taxed again personally. S Corporations avoid double taxation.

- LLC Losses Flow Through to Owners: Can write off financial losses on personal tax returns.

- Corporations Isolate Tax Liability: Shareholders can’t be taxed on entity-level losses.

- LLC Tax Filing Aligns With Personal Deadlines: April 15 for most individual partners.

- Corporations Have Earlier Tax Deadlines: March 15 for S-Corps, April 15 for C-Corps in most states.

LLC Examples:

-

- Mark’s LLC startup losses allowed him writing off $35K invest on his personal Form 1040 filings across 3 years easing tax burdens during lean initial days.

- Traci strategically used an LLC S-Corp election to enable income splitting with her son Billy to minimize their collective tax rates on her thriving consultancy profits.

- Paula distributed uneven LLC dividend payments aligning with each member’s income tax bracket; less to those already earning higher wages from other jobs.

- Chase saved around $5K annually in taxes by choosing LLC pass-through framework instead of standardized C-Corp taxation on his retail startup revenues.

- Jamie avoided substantial double-taxation triggered by profits from Lisa’s inheritance gifted to their joint LLC ownership.

- Mark timed distributions from his LLC to equalize income fluctuation year-over-year smoothing personal tax filing obligations.

Corporation Examples:

-

- Wendy’s corporate profits faced a 25% federal tax rate before 15% taxes again on distributed dividends finally reaching individual hands.

- John’s corporation incurred major losses last year but as 51% owner he couldn’t directly leverage those to offset personal tax liabilities.

- Acme Lighting Corps paid $100K in corporate income taxes prevented from passing through large R&D write-offs to shareholders in a downturn year.

- John’s C-Corp faced triple taxation – corporate income, distributed dividends & capital gain taxes when eventually selling the company.

- Traci saved immensely on taxes when shifting her 10-person company from S-Corp to LLC pass-through structure.

- Chloe was investigating buying Amy’s corporation but balked at locked-in C-Corp taxation complexities complicating exit plans.

How to Proceed:

-

- Analyze multi-year income projections and expected losses before finalizing tax framework.

- Account for issues like ownership splits involving family or inheritance when weighing frameworks.

- Note tax deadline differences to avoid late filings. Keep separate entity vs personal filing dates organized.

- Conduct cost-benefit analysis on LLC tax flexibility vs corporat double taxation scenarios relevant to your business model.

- Take timing considerations like carrying losses forward into future profitable years under varying structures.

- Leave room in decisions to pivot entity type depending on evolving business needs in coming years.

FAQs:

-

- What tax documentation formally establishes an LLC structure? IRS Form 8832 enables selecting C corporation taxation status for IRS purposes. IRS Form 2553 allows for S corporation tax status with the IRS.

- How difficult is it to change LLC partnership taxation down the road? Just file the 2553 electing S-Corp (during the acceptable time frame) or 8832 for C-Corp moving forward. Ensure owners are eligible for S-Corp tax status. LLC operating agreement should also be amended and restated.

- Can I blend LLC with corporate business units under one parent entity? Yes, complex structures allow mixing taxation frameworks across subsidiaries.

- What is the highest corporate tax bracket currently? Max federal corporate tax rate is 21% on income. It’s a flat rate, meaning the same percentage applies to all corporate income, regardless of the amount. This differs from the individual income tax system, which has multiple brackets with increasing rates for higher income earners.

- Do state corporate taxes also apply? Yes absolutely, at lower rates than federal so models must account for combined impact.

- Should ongoing profits factor into framework choice? Yes, phased tax structure shifts can make great sense as companies hit key milestones over time.

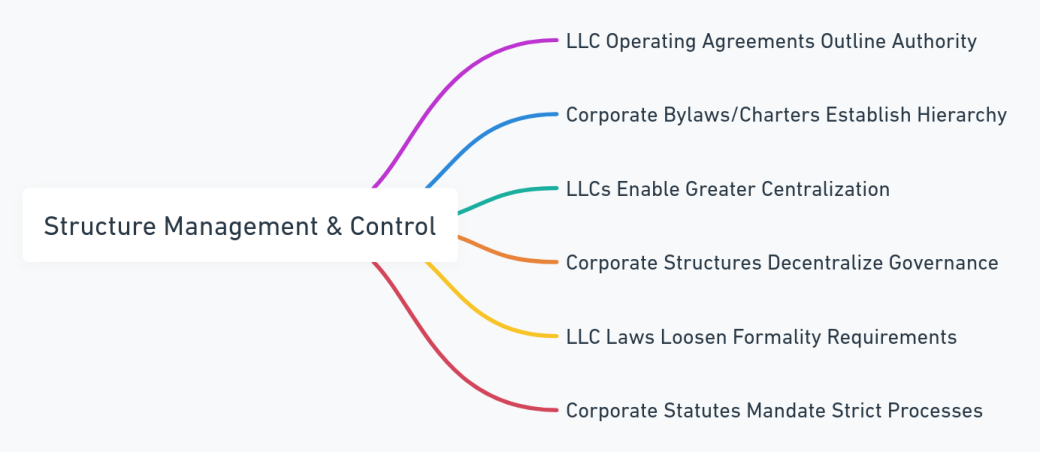

3. Structure Management & Control

-

- LLC Operating Agreements Outline Authority: Customizable to unique needs delegating powers.

- Corporate Bylaws/Charters Establish Hierarchy: Shareholder meetings, officers, boards outline key controls.

- LLCs Enable Greater Centralization: Daily decisions without mandated committees or constituencies.

- Corporate Structures Decentralize Governance: Balancing power through varied leadership entities.

- LLC Laws Loosen Formality Requirements: More flexibility around meetings, votes, documentation needs.

- Corporate Statutes Mandate Strict Processes: Precise procedural rules around governance issues.

LLC Examples:

-

- The Johnsons customized LLC voting exclusively to major asset/debt decisions empowering family managers’ autonomy for daily operations.

- Traci skipped formally documenting director elections relying on oral operating norms among founding LLC partners and key employees informally.

- Aviva easily removed former sales partner Tom per flexible termination provisions in their LLC operating agreement without forcing costly ownership buyback.

- The LLC operating agreement allowed silent angel investor Simon to exit voluntarily without management approval after 6 years securing his principal.

- Amit included mandatory arbitration clauses in the LLC operating agreement to bypass court intervention in internal business disputes.

- The informal LLC structure allowed the Martinez family to rotate management duty yearly based on group votes avoiding outside influence.

Corporation Examples:

-

- Acme Corps mandated appointing independent board directors in formal company bylaws aiming to provide oversight balancing the influential CEO’s power.

- Microsoft empowered public preferred shareholders with rights to directly elect 3 rotating board directors checking substantial control held by founders and executives.

- Yuri followed strict shareholder meeting proceedings letting groups holding 20% stakes formally submit proposals to be considered annually as Corporate Code required.

- snack4U Inc’s corporate bylaws dictated precise processes for calling special impeachment votes of officers failing fiduciary duties.

- The board censured Wheelz Alternatively CEO Gwen when she publicly announced major strategy shifts before required internal procedural approvals.

- Corporate promoter penalties forced Enrique to personally pay $50K for acting on Sports4Life Inc’s behalf without proper authority documented.

How to Proceed:

-

- Consider both centralized vs decentralized styles factoring in founder preferences, outside investor needs and structure flexibility as key decision factors.

- Aim to build consent requirements promoting consultation and shared direction rather than unilateral control wherever possible.

- Balance clear hierarchy on paper with cultivating a collaborative professional culture day-to-day regardless of framework.

- Institute independent director requirements if pursuing venture capital to satisfy investor expectations around accountability.

- Design tie-breaking protocols for major company decisions in advance within operating agreements or bylaw provisions.

- Update controlling documents routinely reflecting mature company needs as founding structures evolve over growth stages.

FAQs:

-

- What authority governs decision making if the operating agreements are silent? Default state LLC partnership laws fill gaps permitting majority votes.

- When are LLC operating agreements traditionally finalized? Best practice has founding partners agreeing to terms when registering the company.

- Can corporate officers ever override board directives? Rarely, executive power remains subordinate other than nominal instances.

- What corporate governance rights can shareholders not sign away? Rights like access to records, attending meetings, voting and electing directors.

- Who formally appoints officers like CEO, COO or CFO in companies? Either shareholders or boards of directors depending on bylaw procedures.

- When are company meeting minutes legally required? Minutes must document and record all official corporate votes and board resolutions.

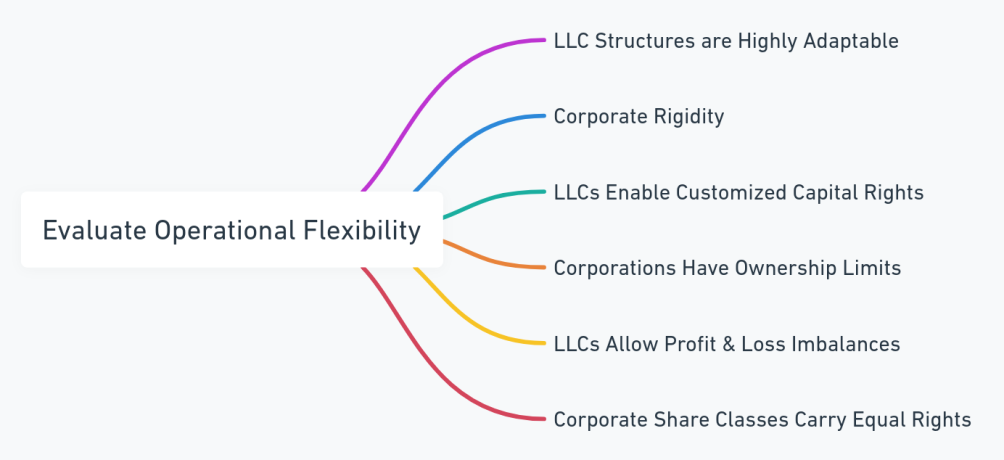

4. Evaluate Operational Flexibility

-

- LLC Structures are Highly Adaptable: Customize capital, control, profit allocation details easily.

- Corporate Rigidity: Locked-in ownership thresholds and constraints on structuring shares.

- LLCs Enable Customized Capital Rights: Structure complex invested capital and debt vehicles flexibly.

- Corporations Have Ownership Limits: 100 shareholder cap for S corporations.

- LLCs Allow Profit & Loss Imbalances: Enable varied distribution models incentivizing key roles.

- Corporate Share Classes Carry Equal Rights: Common stockholders must get equal dividends.

LLC Examples:

-

- The Hopson’s LLC agreement allowed silent angel investor Simon to exit voluntarily without management approval after 6 years just securing back his principal.

- Amit carved out a special class of LLC interests granting board voting rights despite minimal capital investment from directors guiding startup strategy.

- The Martinez family LLC agreement customized family member profit rights based on active operational involvement rather than justownership amounts.

- Pi Analytics issued complex LLC preferred units with 8% preferred returns to key data scientists incentivizing retention despite bigger corporate offers.

- The LLC operating agreement contractually enforced profit distributions despite near-term cash flow crunches at Mehta Marketing Agency.

- DIY Crafts LLC switching to manager-managed governance enabled Kate to focus full-time on design instead of operations without losing decision rights.

Corporation Examples:

-

- Wendys public corporation reached maximum shareholder limit forcing the founder to decide between going public, delisting investors or buying them out.

- Eatable Apps food delivery corporate charter prohibited non-voting common share classes limiting how founders could raise growth capital from Silicon Valley VCs used to leverage.

- Vidcorp’s corporate structure forced equal dividends across common shareholders creating issues incentivizing long-standing creative talent.

- Positive Energy Inc missed key state filing deadlines as C-Corps have less flexibility than LLCs around compliance timing when growth hit unexpectedly.

- Corporate acquisition talks between Vandelay LLC and Kruger Industrial stalled due to small number of owners at the LLC difficult to consolidate into a wider entity.

- Complex earn-out agreement negotiations almost derailed the CorpTex acquisition of competitor Dencil Inc due to less flexible corporate share structures.

How to Proceed:

-

- Analyze scenarios balancing economic incentives, power consolidation and operational disruption under various structures.

- Consider mezzanine-type debt vehicles as hybrid approaches if pure LLC or corporate equity poses challenges attracting capital.

- Incorporate contractual mechanisms or redemption provisions enabling future flexibility even if initial documents are suboptimal.

- Dynamic voting provisions can strengthen minority holders over time tied to milestones balancing near-term vs long-term control.

- Evaluate changes in legal, tax and regulatory treatment of different entities as growth impacts structures.

- Model out 3-5 year scenarios projecting various financing needs and ownership possibilities to determine optimal upfront configurations.

FAQs:

-

- What approvals are needed to amend LLC operating agreements? Default is majority votes though requirements can tighten on key facets.

- What corporate ownership maximums might force public reporting? Thresholds include 2000 shareholders of record and $10M+ gross assets.

- If my LLC will need significant capital should I just incorporate from inception? Not necessarily – choices exist blending LLC and corporate structures under holding company.

- What corporate filings are tied to operational events like mergers? Key documents consist of 8-K material change disclosures.

- Should I consult bankers when crafting shareholder buyout agreements in advance? Wise for setting expectations should future exits, spin-offs or sales arise with built-in complexity.

5. Minimize Administrative Requirements

-

- LLCs Face Fewer Compliance Hurdles: No board governance, shareholder servicing complexities mandated.

- More Onerous Corporate Formalities: Annual meetings, director elections, public filings etc.

- Lean LLC Record-Keeping Requirements: More loosely enforced processes around documentation.

- Strict Corporate Minutes & Resolutions: Detailed proceedings must validate governance actions.

- LLC Statutes Limit Public Disclosure Needs: Finances stay private as ownership remains tight.

- More Corporate Financial Transparency: Investors often mandate audits, performance reporting.

LLC Examples:

-

- Traci’s LLC operating agreement allowed skipping formal management votes as long as unanimous partner consent on major company decisions.

- Family LLC counsel advised limited documentation of asset transfers and profit distributions between members and company to restrict potential tax audits.

- The informal LLC structure allowed the Chens delegating daily decisions to rotating family managers without prescribed oversight procedures.

- Paula’s single-member LLC only required simple filings upon dissolution rather than extensive shareholder communications and liquidation proceedings.

Corporation Examples:

-

- Acme Lighting enforced quarterly board meetings prolonging decision-making with mandated fiduciary procedures around major spending proposals.

- Public shareholders compelled Vidcorp to undergo comprehensive financial statement audits annually at steep accounting fee costs.

- Formal corporate dissolution forced extensive layoff notifications, creditor payment priority planning, and asset appraisals before Blue Strawberry Inc could close up.

- Corporate merger requirements had ShopCartDevelopers filing multiple state Forms, publications, and shareholder issuances complicating the acquisition.

- MicroManager Inc’s corporate records failed to substantiate CEO selections upon IRS audit resulting in penalties for improperly filed taxes.

- DentalCorp infringement settlement terms mandated new incident reporting procedures and internal claim controls per formal directors’ orders.

How to Proceed:

-

- Compare lost opportunity costs of decision delays under various structures factoring growth pace, complexity.

- Consider streamlined entities at inception but build processes scalable if investors/ public shareholders eventually expect transparency.

- Shift more centralized oversight as operations mature requiring added controls – document accordingly.

- Model projected public filing, audit and liability insurance costs tied to heightened governance requirements.

- Factor reputational risks around financial reporting and compliance discipline into structural decisions.

- Consult legal experts on administrative intricacies around ownership transfers, dissolutions under alternate structures.

FAQs:

-

- What are allowable information exclusions under LLC reporting? Taxes, distributions, salaries, and revenue metrics can stay undisclosed.

- Do single-shareholder corporations require governance documentation? Less critically but still prudent especially if seeking future outside investment.

- Can informal records like texts qualify as corporate minutes? No, minutes have precise legal formatting standards around meeting protocols.

- What dissolution reporting applies to LLCs? Certificate of Cancellation just discloses formal termination of entity and registration.

- Who sets corporate disclosure requirements publicly? SEC mandates filings like 10-Qs, 10-Ks, 8-Ks for shareholder communications.

- Should administrative hassles guide structure over economics? Wise to model costs but generally better optimizing flexibility and incentives.

6. Compare Financing Strategies

-

- LLC Challenges Attracting Investors: Confusion around taxation, little ownership tracking.

- Corporate Structures Built For Raising Capital: Share sales, IPOs, preferred stock channels access extensive funding.

- LLCs Offer Less Loss Protection For Investors: Greater risk around fraud/poor management with minimal oversight.

- Corporations Require More Stringent Governance: Appeal to investors wanting transparency protections on their capital.

- LLCs Allow Flexible Investor Exits: Redemption agreements can customize liquidation rights.

- Corporate Share Sales Subscribe To Standards: Common conventions around tradeability, control valuations.

LLC Examples:

-

- The Hopsons struggled attracting VC without projected share sales, requiring simpler debt vehicles like loans and convertible notes instead for their startup.

- Paula’s friends expressed wariness investing in her LLC yoga business without financial statements, protections against personal asset mixing.

- Kate’s custom redemption agreement clauses enabled her brother’s minority LLC stake buyback when relocating abroad at a pre-set discounted formula price.

- Amit secured LLC financing from a family office given the bespoke preferential distribution rights without market standards influence.

- The Chen’s offered varying LLC profit splits allowing different investment amounts from each sibling based on individual risk tolerances.

- CCrporation merger discussions between Vandelay LLC and industry competitor stalled over individually negotiating dozens of distinct LLC owner payouts.

Corporation Examples:

-

- Emily easily attracted seed funding from angel investors via standardized preferred corporate stock issuance vs complex LLC agreements.

- Corporate venture capital backed Wendy’s mobile platform buying convertible notes eventually exchanged for common shares.

- Yellow Pages incumbent acquired emerging local search rival NeighborhoodFeed Inc via customary public company buyout process.

- Jay took his telehealth corporation public raising substantial growth capital via an SEC-regulated IPO.

- After CableNet Inc’s market cap crossed $50 million, early employees readily sold vested shares as standard public stock options.

- As corporate director, Fran had fiduciary duties protecting minority shareholder rights influencing market transparency.

How to Proceed:

-

- Model multi-round financing needs and factor probability securing each structure’s capital channels.

- Double check tax implications for global investors under pass-through entities to avoid surprises.

- Consider mezzanine type debt/equity blends if struggling structuring pure common/preferred stock or membership unit rounds.

- Evaluate ability to scale complex LLC investor relations vs more standardized public listings before commitments.

- Enhance LLC governance/financial transparency to strengthen minority owner protections countering structural weaknesses.

- Plan exit scenarios evaluating options facilitating future sale/IPO under each framework.

FAQs:

-

- What investor protections exist for LLC minority owners? Mainly duties of care and loyalty imported by state partnership statutes.

- Can LLC ownership be traced publicly like corporations? No, less transparency around budgets, identities, contributions.

- What corporate capitalization paths facilitate late-stage exits? Tradable public stock, disclosure requirements attractive to acquirers.

- Do SEC regulations apply to LLC fundraising? Only if deemed public investment vehicles, otherwise exempt.

- Why don’t VCs like complicated LLC agreements? Harder assessing value, lack minority protections, limit exit optionality relative to corporate terms.

- Can LLC founders easily regain control post-investment like corps? Yes via voting rights/allocations customized in operating agreements.

7. Ensure Business Continuity

-

- LLC Life Span Tied to Members: Can dissolve without succession plans when key players exit.

- Corporations Persist Through Ownership Changes: Withstand loss of shareholders/executives.

- Narrow LLC Ownership Creates Risk: Death/retirement triggers can force unwinds.

- Corporate Perpetuity Powers Legacy Building: Outlasts individual stakeholders.

- Poor LLC Succession Planning Causes Issues: Contract omissions can enable serious dysfunction.

- Corporate Structure Smooths Leadership Changes: Hierarchy sustains operations through transitions.

LLC Examples:

-

- Mark’s sudden CEO retirement forced his 50-person company into voluntary dissolution without mapped successors or plans partitioning leadership.

- Unclear decision authority post-departure left Jane’s LLC unable to renew major client contracts or pivot strategies lacking consensus.

- Traci’s outdated LLC agreements transferred 2 deceased partners’ full interests to uninvolved heirs unable to agree on direction.

- The Chen family LLC nearly folded when parents retired after kids couldn’t agree on leadership models going forward.

- John retired early from FirstAccess LLC thinking his son would inherit management rights per agreements, only to find outdated clauses had lapsed.

- The Nguyen’s missed major expansion opportunities trapped in years of court proceedings after a founding brother passed without updated buyout terms.

Corporation Examples:

-

- Microsoft smoothly replaced CEO’s over decades with planned transitions between supporting management layers sustaining growth.

- The Warner Brothers entertainment empire continued for 120+ years despite heirs only retaining nominal ownership thanks to corporate perpetuity.

- Fashion Inc never halted operations during a bitter public lawsuit between co-founders with independent continuity infrastructure in place.

- McDonalds maintained excellence after Ray Kroc’s passing given corporate mechanisms to systematically transfer knowledge/contacts to rising leadership.

- Ford Motors survived the unexpected death of heir apparent Edsel Ford in 1943 with deep roster of directors and senior managers prepared to lead.

- Coca-Cola’s strong corporate brand and governance enabled growth for a century despite massive senior executive turnover.

How to Proceed:

-

- Map leadership/training pipelines to groom next generation well before today’s decision makers plan departures.

- Create LLC transfer and buyout protocols contractually protecting continuity when inevitable ownership changes arise.

- Regularly refresh operating agreements to ensure continuity provisions still make sense for evolving businesses over time.

- Consider independent governance structures balancing family politics across generations if pursuing multi-generational LLC ventures.

- Model various leadership loss scenarios analysing risks of corporate instability – plan mitigations accordingly.

- Study mechanisms like perpetual purpose trusts if aiming to build corporations sustaining your legacy for long horizons.

FAQs:

-

- What happens to LLC assets lacking dissolution provisions when members exit? Courts order distributions per state rules often unevenly.

- Can LLCs elect perpetuity after key members depart? Yes via replacement mechanisms but needs advanced consent.

- What approvals need continuity plans mapped out well in advance? Major events like mergers, capital raises requiring decisions.

- How are corporate shares managed when stockholders pass away? Transferred to designated beneficiaries avoiding disruption.

- What issues arise transferring LLC stakes to uninvolved heirs? Inheriting beneficiaries potentially unqualified or adversarial.

- Can shareholders be completely replaced while the corporation persists forever? Yes, equity transferred freely overtime while entity continues.

8. Structure for Future Exits

-

- LLCs Have Innate Challenges Attracting Acquirers: Highly customized membership agreements require complex deal-by-deal negotiations further complicating transactions.

- Corporations Built to Streamline Ownership Transfers: Standardized, publicly traded securities greatly aid post-IPO share sales or structured private entity mergers.

- LLCs Lack Secondary Markets For Trading Ownership Stakes: No straightforward mechanisms enabling disjointed owners to efficiently exchange complex company interests.

- Public Corporate Share Liquidity Enables Flexible Transitions: The ability to readily trade stocks, bonds and options simplifies future leadership transitions.

- Tax Impacts Vary Substantially on LLC Sales: Pass-through structure means profits get taxed differently depending on what forms acquirer mergers take and divisions of retained equity vs exited payout portions.

- Extensive Public Value Metrics Empower Corporate Transactions: Market information aids negotiations leveraging extensive financial analytics to optimize acquisition terms for tax efficiency.

LLC Examples:

-

- The Hopsons struggled exiting their LLC as complex member agreements required slow individual negotiations versus standardized corporate share sales.

- Traci fitness tried taking on LLC equity investors but partners balked at increased acquisition complexity down the road hampering eventual exit options.

- Years negotiating dozens of distinct LLC stake payouts halted the $100M sale of Blue Strawberry coffee to a specialty retail giant interested in just the trade name.

- The majority LLC owner avoided paying fair buyout prices upon retirement given challenges minority holders faced banding together to bargain without established market value data.

Corporation Examples:

-

- Emily drew multiple public acquisition bids due to the clear cap table transparency from early stage preferred stock sales to angel investors under a corporate model.

- VC-backed corporation DentalCloud pursued an IPO enabling $300M+ in early employee/investor cashouts without requiring individual stake negotiations.

- Haymaker Bros was acquired seamlessly via a standard corporate merger transaction by a Fortune 500 hospitality company seeking to expand into boutique inns.

How to Proceed:

-

- Analyze long term capital needs factoring ability for equity holders to access liquidity under each structure considering exit paths.

- Model tax costs from asset sales, diverse merger variations and IPOs as LLC structures can complicate planning relative to public corps.

- For LLCs needing outside funding, set redemption schedules contractually protecting eventual exit leeway avoiding full locked-in arrangements.

- Evaluate likelihood of pursuing standard mergers, acquisitions or public listings down the road before selecting structures limiting flexibility.

FAQs:

-

- Are minority LLC owners contractually obligated to accept any acquisition offers approved by majority vote? Defaults to yes unless agreements explicitly carve out additional approval rights.

- What corporate capitalization paths best support ambitions of eventually going public? Venture rounds issuing standard preferred stocks with IPO conversion rights upon maturation.

- How are LLC merger discrepancies resolved if some owners want to remain invested while others wish to exit fully? Requires extensive negotiations – no clean mechanisms.

- Can corporations force buying out common shareholders if board approves an acquisition deal? Yes, via default drag-along rights pushing uniform decisions.

- What downside risks emerge from LLC partner disputes overseeing major asset sales? Courts dictating intervention outcomes despite lacking business operational familiarity.

- Do public markets increase probabilities of companies eventually getting sold? Yes, ample data transparency and liquidity options enable ideal outcomes for interested acquirers.

Summary

Choosing between LLC and Corporate structures constitutes one of the most critical early decisions arising when building a business.

Carefully weighing factors like liability protection, taxation frameworks, governance customization, compliance overheads, branding control and investor exit levers ultimately empowers entrepreneurs optimizing foundations for growth.

LLCs provide unmatched flexibility particularly around bespoke agreements dividing management authority, profits and assets among partners.

However more complex interstate expansions, fundraising needs and leadership transitions can challenge continuity absent standardized corporate infrastructure.

Model projected scenarios analyzing how both structures accommodate likely evolution stages in your industry. Seek counsel bridging advisors knowledgeable on state-specific norms if aiming for regional breadth.

Ultimately prioritize building in upfront governance mechanisms able to sustain operations through unpredictable environments.

Thoughtfully addressing front-end structural considerations today paves avenues enabling your dreams of launching an enduring, prosperous enterprise come true for many tomorrows ahead.

Move ahead confidently by deliberately optimizing essential legal frameworks now so you can concentrate on executing business growth free of avoidable distractions later.

Need Help Choosing Between LLC vs Corporation?

Contact us to be connected with a business law attorney who can analyze your unique situation and projected plans providing tailored guidance around optimal legal entities to establish your promising startup or growing small business.

Test Your LLC vs. Corp Knowledge

Section 1: Limit Personal Liability

Questions:

-

- 1. Which business structures offer protection against personal assets being targeted?

- A) Sole proprietorships

- B) General partnerships

- C) Limited liability companies

- D) Corporations

- 2. What legal concept allows courts overriding LLC liability protections?

- A) Promoter penalties

- B) Successor clauses

- C) Piercing the corporate veil

- D) Private equity exemptions

- 3. Why buy dedicated D&O insurance for corp shareholders and execs?

- A) Avoid double taxation

- B) Enable loss write-offs

- C) Lower administrative costs

- D) Mitigate liability exposures

- 4. What legal provision best reinforces liability limitations?

- A) Non-voting stock

- B) Indemnity clauses

- C) Restrictive agreements

- D) Written liability statements

- 5. What scenario risks reversing liability protections?

- A) Tax delinquencies

- B) Loan defaults

- C) Undercapitalization

- D) Slow growth

- 1. Which business structures offer protection against personal assets being targeted?

Answers:

-

- 1. C & D – Limited liability companies structure explicitly prevents owners’ personal assets being targeted for business liabilities and debts. C Corporations also provide liability protection.

- 2. C – “Piercing the corporate veil” represents the legal concept allowing courts overriding liability protections if serious misconduct emerges.

- 3. D – Though more expensive upfront, D&O policies directly address residual liability risks corporate directors and officers still retains despite entity structures.

- 4. D – Codifying limited liability for owners explicitly within operating agreements and bylaws reinforces protections against future creditor claims.

- 5. C – Undercapitalizing companies risks reversing liability shields if suggesting deliberate misconduct rather than distinct entity status.

Section 2: Explore Tax Considerations

Questions:

-

- 1. What tax election lets LLCs choose corporate taxation?

- A) Form 1065

- B) Form 8832

- C) Form 1120

- D) Form 2553

- 2. Which structure enables direct pass-through of financial losses?

- A) C corporations

- B) S corporations

- C) Non-profits

- D) LLCs

- 3. What tax deadline applies to LLC pass-through filings?

- A) March 15

- B) April 1

- C) April 15

- D) Oct 15

- 4. How are S-Corp shareholder taxes handled relative to C-Corps?

- A) Lower capital gains rates

- B) Eliminate double taxation

- C) Increase personal exemptions

- D) Claim more deductions

- 5. What impacts choice between LLC tax status vs corps?

- A) Profit predictions

- B) State of incorporation

- C) Location of shareholders

- D) All of the above

- 1. What tax election lets LLCs choose corporate taxation?

Answers:

-

- 1. B – IRS Form 8832 allows LLCs electing taxation as C corporations going forward as needed.

- 2. D – The innate LLC pass-through framework transfers company financial losses directly onto personal owner tax returns.

- 3. C – Most LLC partnership tax returns align with April 15th individual filings deadlines since profits flow through to owners.

- 4. B – The S-Corp election avoids C corps’ double taxation of assets sold and dividends issued to shareholders.

- 5. D – Current and projected profit levels, states of registration and owner locations all significantly impact choice between LLC tax status vs corps.

Section 3: Structure Management & Control

Questions:

-

- 1. What provisions govern LLCs lacking operating agreements?

- A) State corporate law

- B) LLC act statutes

- C) Partnership common law

- D) Non-profit conventions

- 2. What board formalities are legally required of corporations?

- A) Annual meetings

- B) Public reporting

- C) Leadership diversity

- D) Committee charters

- 3. What provisions can LLC agreements customize?

- A) Profit allocations

- B) Buyout terms

- C) Voting structures

- D) All of the above

- 4. What statutory filings detail significant corporate events?

- A) 8-Ks

- B) 10-Qs

- C) Proxy statements

- D) Annual reports

- 5. Can LLCs accommodate both centralized and decentralized styles?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 1. What provisions govern LLCs lacking operating agreements?

Answers:

-

- 1. B – Absent operating contracts, default LLC partnership statutes set baseline decision protocols.

- 2. A – Annual shareholder meetings mark only formal universal legal requirement for corporate boards.

- 3. D – LLC operating agreements enable broadly customizing profit splits, buyouts, voting authority and more.

- 4. A – Public companies use 8-K filings detailing material leadership changes, mergers and major asset sales.

- 5. A – Yes, LLC agreements can concentrate authority or decentralize powers across partners/committees.

Section 4: Evaluate Operational Flexibility

Questions:

-

- 1. What requirements restrict S-Corp ownership?

- A) Accredited investors

- B) US citizens

- C) Industry experience

- D) Shareholder caps

- 2. What corporate document outlines leadership hierarchy?

- A) Operating agreement

- B) Corporate charter

- C) Bylaws

- D) LLC act

- 3. Can LLC agreements override some default laws?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 4. What requires corporations share dividends equally?

- A) SEC rules

- B) Shareholder votes

- C) Common stock rights

- D) Annual report filings

- 5. Can LLC agreements specify unique exit terms?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 1. What requirements restrict S-Corp ownership?

Answers:

-

- 1. D – The IRS limits S-Corp shareholders to 100 accredited investors only, capping ownership control options.

- 2. C – Corporate bylaws formally designate board seats, officers and structural hierarchy procedures.

- 3. A – Yes, LLC operating agreements can override state partnership act default provisions contractually.

- 4. C) – Common shareholders rights require equal dividends distributions relative to ownership stakes.

- 5. A – LLC agreements enable prescribing specific exit clauses, buyback terms and control provisions for partners.

Section 5: Minimize Administrative Requirements

Questions:

-

- 1. What records can LLCs exclude from public reporting?

- A) Ownership stakes

- B) Tax liabilities

- C) Profit distributions

- D) All of the above

- 2. What SEC regulations mandate public company reporting?

- A) Regulation D

- B) Regulation A

- C) Regulation S-X

- D) Regulation S-K

- 3. What records can LLCs maintain more informally?

- A) Meeting minutes

- B) Asset registers

- C) Resolutions

- D) All of the above

- 4. What dissolution filing details LLC asset distributions?

- A) Certificate of cancellation

- B) Articles of dissolution

- C) Statement of resolutions

- D) Ownership transfer ledger

- 5. Do single-owner LLCs require governance documentation?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 1. What records can LLCs exclude from public reporting?

Answers:

-

- 1. D – LLC statutes broadly exclude financial metrics like ownership, taxes and distributions from public reporting.

- 2. D – SEC Regulation S-K defines disclosure requirements for public companies around risk factors, MD&A, compensation etc.

- 3. D – Meeting minutes, asset registers and formal resolution processes can stay quite informal under LLC flexibility.

- 4. A – The Certificate of Cancellation discloses LLC dissolution and concludes outstanding registration matters simply.

- 5. C – Single owner LLCs warrant some best practice documentation, especially if later pursuing outside investors.

Section 6: Compare Financing Strategies

Questions:

-

- 1. What characteristic complicates valuing LLC stakes?

- A) Customization

- B) Tax treatment

- C) Ownership caps

- D) State limitations

- 2. What financing path best supports pursuing an IPO?

- A) Venture rounds

- B) Commercial loans

- C) Convertible notes

- D) Crowdfunding

- 3. Why don’t VCs prefer complex LLC agreements?

- A) Limit exit options

- B) Ownership caps

- C) Lower valuations

- D) Restrict preferences

- 4. How can LLC gaps attracting investors be addressed?

- A) mezzanine debt vehicles

- B) Focusing on Angels not VCs

- C) Enhancing financial transparency

- D) All of the above

- 5. What exit rights should LLC agreements specify?

- A) Redemption schedules

- B) Company sale vetoes

- C) Private equity takeover approvals

- D) Leader departure buyouts

- 1. What characteristic complicates valuing LLC stakes?

Answers:

-

- 1. A – Highly customized LLC agreements complicate documenting comparable valuation metrics appealing to outside investors.

- 2. A – Venture capital preferred share rounds best position companies for eventual IPO transitions when startup phases conclude.

- 3. A – VC firms prefer more standardized corporate structures better supporting various future investor exit strategies.

- 4. D – Hybrid debt/equity vehicles, Angels over VCs and added reporting transparency together can strengthen LLC capital fundraising.

- 5. D – Codifying leadership buyout rights contractually provides investor continuity protection given LLC perpetuity uncertainties.

Section 7: Ensure Business Continuity

Questions:

-

- 1. What poses continuity risks to LLC viability long-term?

- A) Undercapitalization

- B) Equity restrictions

- C) Key partner loss

- D) Board dynamics

- 2. What enables corporations outlasting individual leaders?

- A) Perpetual purpose

- B) Ongoing innovation

- C) Brand resilience

- D) Culture preservation

- 3. What LLC clauses promote leadership transitions?

- A) Goodwill provisions

- B) Mandatory training

- C) Performance metrics

- D) Buy-sell agreements

- 4. How do corporations handle shares post-death events?

- A) Redeem automatically

- B) Allow transfers

- C) File dissolution

- D) Enact clawbacks

- 5. Can corporations survive full ownership turnover?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state law

- 1. What poses continuity risks to LLC viability long-term?

Answers:

-

- 1. C – Losing key LLC partners can threaten continuity lacking standard corporate succession protocols.

- 2. A – The perpetual existence tenet of corporations enables them outlasting any given executive or shareholder.

- 3. D – Codifying leadership buyout terms contractually sustains LLC operations through inevitable partner transitions.

- 4. B – Corporate shares automatically transfer to designated heirs upon stockholder death without need for entity dissolution.

- 5. A – Yes, corporations can absolutely survive complete turnover of equity owners while continuing business operations.

Section 8: Structure for Future Exits

Questions:

-

- 1. Why is selling LLC ownership stakes challenging?

- A) High customization

- B) Tax uncertainties

- C) Strict investor caps

- D) Low profitability

- 2. How do public stocks enable leadership transitions?

- A) Tradeability

- B) Dividend priorities

- C) ROFR waivers

- D) IPO carve outs

- 3. What mechanisms facilitate corporate acquisitions?

- A) Financial transparency

- B) Standard agreements

- C) Leadership protections

- D) Ownership flexibility

- 4. How can LLC exit limitations be addressed upfront?

- A) Contractual put options

- B) Mandatory redemptions

- C) Leadership incentives

- D) Independent valuations

- 5. What rights help protect against LLC exit exploitation?

- A) Supermajority approvals

- B) Mandatory distributions

- C) Independent appraisals

- D) Leadership stability requirements

- 1. Why is selling LLC ownership stakes challenging?

Answers:

-

- 1. A – Highly customized LLC agreements necessitate complex individual deal negotiations hampering investment exits.

- 2. A – Public stock tradeability gives retiring executives and employees options cashing out ownership smoothly following IPO transitions.

- 3. B – Standard stock sales contracts, shareholders agreements streamline corporate mergers, acquisitions logistically.

- 4. D – Independent valuations contractually protect minority stakeholders from exploitation if future LLC sales arise with limited external value data available.

- 5. C – Fair independent appraisals prevent majority investor coercion around purchase terms during LLC ownership transfer events.

Also See

Incorporating Your Business the Right Way: The Entrepreneur’s Handbook

Disclaimer

The LLC and corporate business structure information presented in this article is for general educational and guidance purposes only and does not constitute formal legal or tax advice. We recommend directly contacting an experienced business formation lawyer licensed in your state for professional advice tailored to your unique operational situation and strategic growth plans when evaluating LLCs, corporations, share issuances, taxes and regulatory compliance.