C corporations face the burden of double taxation where income gets taxed once at the corporate level and again through dividends distributed to shareholders. S corporations receive pass-through tax treatment avoiding this issue by passing all profits/losses directly to owners’ personal returns. Shareholders then pay taxes at individual rates on those subsequent distributions.

This pass-through model also applies to LLCs, partnerships and sole proprietorships as conduits flowing income straight to members’ 1040s. However, formally electing S corporation status unlocks additional tax benefits not available to those other entities like payroll and fringe benefit tax savings plus specialized credits.

This comprehensive guide unpacks the many advantages of S corps around mitigating tax burdens including:

1) Avoiding double taxation 2) Optimizing payroll tax liability 3) Writing off fringe benefits 4) Leveraging tax credits and deductions 5) Carrying operating losses forward 6) Accelerating equipment depreciation 7) Qualifying for qualified business income (QBI) deductions 8) Expensing home office spaces 9) Streamlining compliance requirements.

Unpacking each opportunity empowers small business owners to maximize savings while maintaining operations. Let’s explore the key benefits unlocked by this IRS classification election.

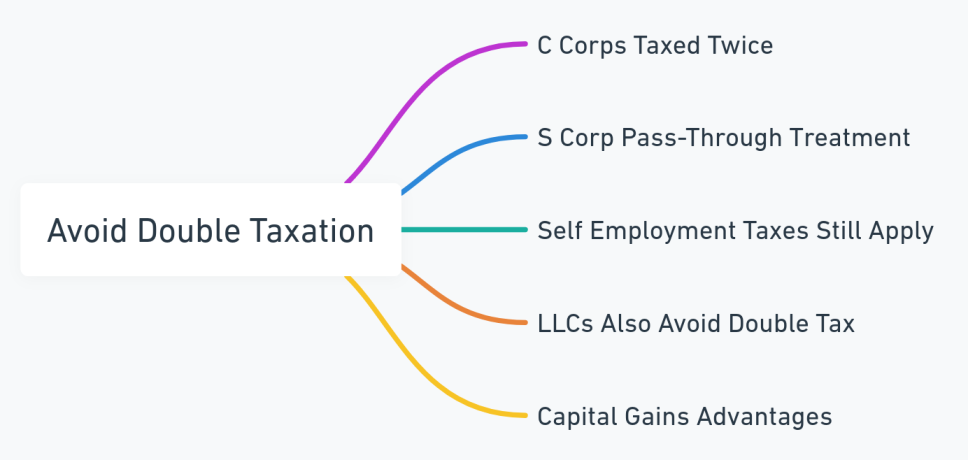

1. Avoid Double Taxation

-

- C Corps Taxed Twice: Once at corporate rates then shareholders owe individual taxes on distributed dividends.

- S Corp Pass-Through Treatment: Income flows directly to shareholders’ personal returns taxed there avoiding double tax.

- Self Employment Taxes Still Apply: Shareholders pay 15.3% FICA taxes on their K-1 pass through share.

- LLCs Also Avoid Double Tax: But may face state fees and limitations S corps don’t.

- Capital Gains Advantages: S corp investors enjoy lower rates on proceeds from appreciated asset sales.

Example:

-

- Wendy’s S corp income flows through to her Form 1040 taxed once at individual rates whereas C corp dividends face double taxation.

- The $100K pass through saves federal corporate income taxes but Wendy pays self employment taxes on those earnings.

- LLCs also avoid double corporate tax but ownership structures face more restrictions.

- Selling appreciating assets like IP down the road may qualify for deferred lower capital gains rates.

- Both S corps and LLCs share pass through single layer taxation benefit.

How to Proceed:

-

- Model tax scenarios projecting C corp vs S corp election savings amounts.

- Verify state taxation policies conform with federal pass through guidelines.

- Consider long term exit strategies when evaluating entity structures upfront.

- Factor additional payroll burdens assessed on pass through shareholder wages.

- Discuss personal financial situations with CPAs ensuring S corp or LLC fit needs best.

FAQs:

-

- Does pass through status apply to revenue from international operations? Yes, global revenue flows through to US shareholders’ returns.

- Can deductible S corp losses offset owners’ other tax liabilities? Yes, pass through losses offset shareholders’ income from investments, W-2 wages, etc.

- What if only some owners actively work for the S corp – how are taxes handled? All shareholders pay taxes on K-1 pass through income regardless of employee status.

- Do LLCs and S corps both avoid corporate double taxation permanently? No, S corps can elect C status and pay entity level taxes while LLCs face fewer restrictions.

- Can valuation discounts reduce capital gains taxes on asset sales for S corps? Yes, lack of control and marketability discounts may apply lowering taxable gain.

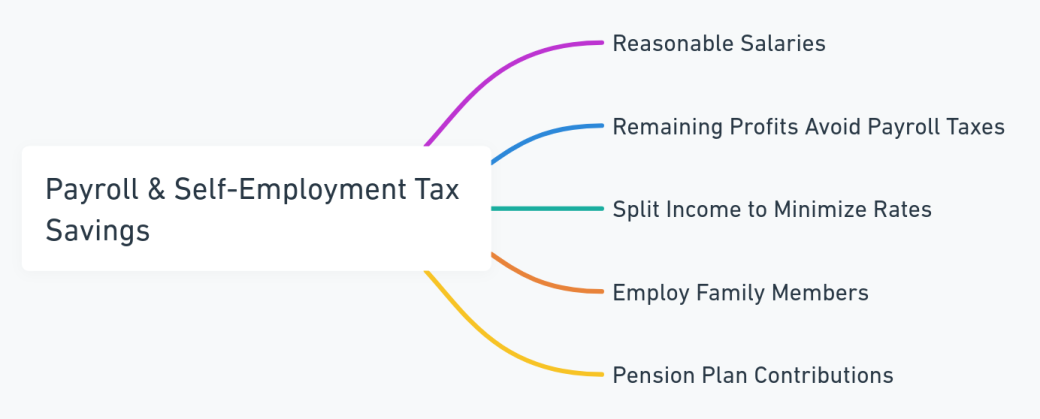

2. Payroll & Self-Employment Tax Savings

-

- Reasonable Salaries: Owners must pay themselves fair salaries as employees subject to payroll taxes.

- Remaining Profits Avoid Payroll Taxes: Distributions beyond W-2 wages avoid 15.3% levies.

- Split Income to Minimize Rates: File jointly and allocate across lower tax bracket spouse.

- Employ Family Members: Pay reasonable wages to relatives too, expanding savings.

- Pension Plan Contributions: Defer taxes by funding retirement accounts.

Example:

-

- Tom paid himself $60K salaries from his S corp avoiding $30K in payroll taxes on the $90K balance distributed as dividends.

- His spouse Mary earned $30K so they split the $90K dividends across returns lowering their tax bracket exposure.

- Hiring their teenagers part time at reasonable summer job wages expanded tax savings by $5K.

- Tom also deferred taxes paying 25% of the dividends into Solo 401k retirement accounts.

- Reasonable wages combined with income splitting and retirement funding strategies provided major tax savings.

How to Proceed:

-

- Compare and set salary levels aligning with similar roles and qualifications.

- Model income allocation across filing statuses and brackets to optimize.

- Evaluate employing family members balancing reasonable pay vs tax savings.

- Consider bunching tax liabilities year over year with alternating profit distribution/pension funding strategies.

- Annually assess earned income vs distribution levels as business conditions evolve.

FAQs:

-

- Can I adjust salaries whenever without IRS scrutiny? No, amounts should align consistently based on duties and benchmarks.

- What if I contribute over limits into retirement accounts accidentally? Excess amounts get taxed at 6% and carry forward hitting future caps first.

- Do I owe payroll taxes on annual income regardless of timing distributed? No, levies apply solely on W-2 salary amounts, not later dividends.

- Can an S corp pay health insurance instead of salaries to owners? No, reasonable wages must be paid covering performed duties.

- Do underage children owe income taxes on any wages I provide them? Generally earned income over $12,400 gets taxed for dependents.

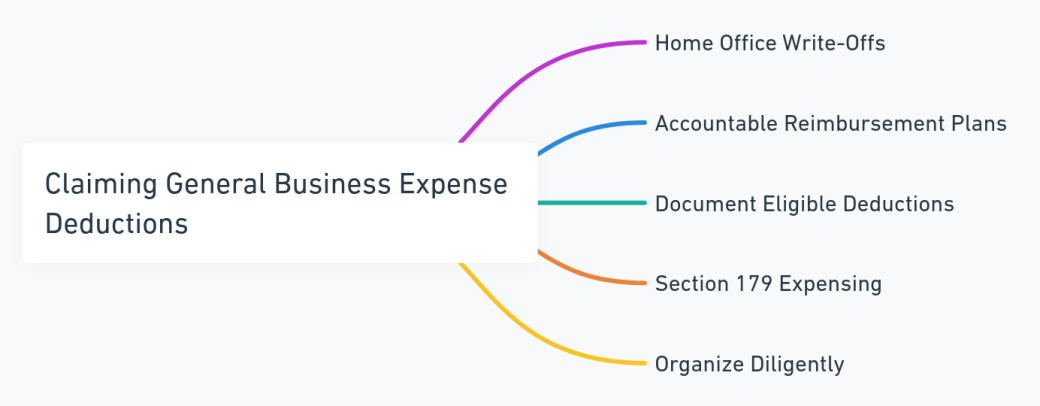

3. Claiming General Business Expense Deductions

-

- Home Office Write-Offs: Deduct portion of housing costs associated with dedicated workspace.

- Accountable Reimbursement Plans: Pay employees back certain expenses tax free.

- Document Eligible Deductions: Travel, utilities, supplies and other ordinary costs.

- Section 179 Expensing: Fully deduct certain assets like equipment first year.

- Organize Diligently: Keep immaculate records to prove write-off eligibility if audited.

Example:

-

- Jim deducted 20% of his home costs associated with the dedicated office space used daily to manage his S corp.

- He also formally tracked mileage logs qualifying the reimbursements under accountable plan rules.

- Purchased equipment like computers also qualified for full Section 179 deductions.

- Careful bookkeeping organized all eligible business expenses clearly tied to operational activities.

- Diligent documentation supported write-offs claimed across multiple categories on the S corp returns.

How to Proceed:

-

- Consult IRS guidelines closely tracking home office deduction qualifications.

- Set clear accountable plan reimbursement policies aligned with federal regulations.

- Consider expense tracking systems automatically importing and backing up documentation.

- Take Section 179 deductions up to annual expensing limits early on asset lives.

- Take pictures documenting purchases in case receipts get misplaced.

FAQs:

-

- What methods can claim vehicle expenses? Standard mileage or actual costs like fuel, insurance, depreciation.

- Do expense limits adjust with inflation over time? Yes, 179 deduction caps and mileage rates update periodically.

- Can accountable plans reimburse services beyond hard goods? Yes, travel, internet and phone can qualify.

- Are passive investors eligible for expense write offs? Rarely, deductions require active involvement in the business.

- What constitutes acceptable home office documentation? Pictures, diagrams, time logs etc. proving exclusive regular business use.

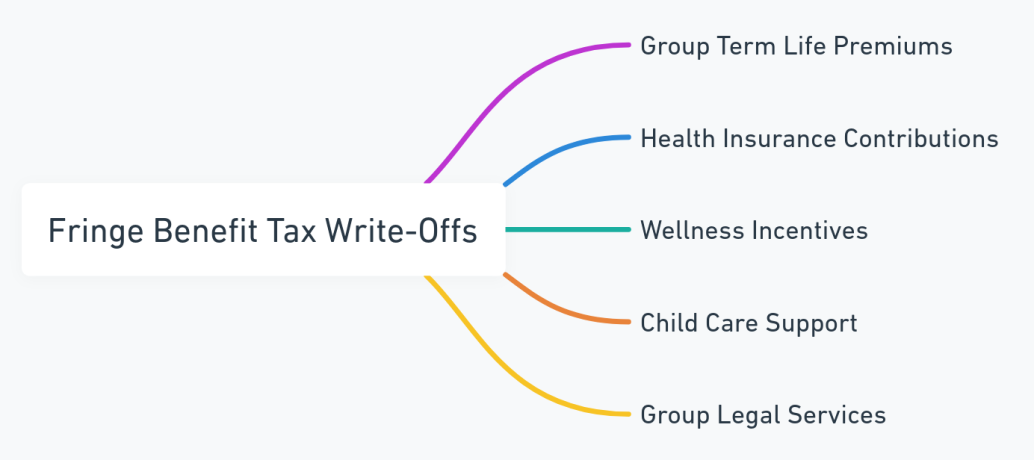

4. Fringe Benefit Tax Write-Offs

-

- Group Term Life Premiums: Deduct costs covering up to $50K death benefits per employee.

- Health Insurance Contributions: Certain plans like HSAs, FSAs provide write-offs.

- Wellness Incentives: On-site gym access or reimbursement programs qualify.

- Child Care Support: Providing facilities or subsidies can be deducted.

- Group Legal Services: Assisting employees with wills, real estate closings etc.

Example:

-

- Acme Corp funded $1K per employee towards membership fees at a nearby gym promoting fitness.

- They deducted $8K annually covering premiums on supplemental life insurance policies.

- HSA contributions provided medical insurance write-offs.

- Onsite childcare services subsidized costs for working parents.

- Free annual legal consultations assisted employees with personal matters like estate planning.

How to Proceed:

-

- Review program criteria ensuring compliance with IRC Sections on qualified benefits.

- Compare multiple medical insurance plan options balancing premiums against offered features.

- Formalize reimbursement request processes for consistency across recipients.

- Take advantage of fringe benefit programs boosting recruitment, retention and morale too.

- Get professional advice tailoring offerings that maximize value for owners and staff.

FAQs:

-

- What are eligibility requirements to receive these tax-free benefits? Typically full-time W-2 employee status.

- Must I offer the same benefits to all employees and owners? Generally yes, but some variance allowed based on compensation tiers.

- Can I deduct health insurance premiums paid for family members? Yes, spouses and tax dependents also qualify under rules.

- Are reimbursed gym fees considered taxable income? No, not if program structured as accountable fringe benefit.

- What are the tax implications of group legal service benefits? No income taxes owed by employees, S corp deducts costs.

5. Specialized Industry Credits & Deductions

-

- R&D Tax Credits: Up to 10% credit on qualified research expenses and activities.

- Domestic Production Activities: 9% deduction on income from US manufacturing, software production etc.

- Film/TV Write-Offs: Deduct production expenses in year paid under Sec 181 rules.

- Cost of Goods Sold Treatment: Certain industries subtract inventory inputs from gross receipts.

- Biodiesel Credits: $1/gallon produced, blenders claim $.50/gallon blended.

Example:

-

- Acme Transportation’s logistics software R&D qualified for tax credits offsetting liability.

- Precision Manufacturing deducted material and production costs before recognizing taxable income.

- Biodiesel producer New Wave Energy claimed $1 per gallon in alternative fuel tax credits.

- 911 Pictures excluded film production expenses from taxable proceeds avoiding losses.

- Tailored industry rules subsidized research, manufacturing, energy and entertainment ventures.

How to Proceed:

-

- Determine eligibility for any niche programs benefiting sector-specific initiatives.

- Maintain thorough documentation proving activities satisfying complex statutory rules.

- Consider IRS pre-approval applications providing certainty around credits claimed.

- Apply conservative interpretation of grey area qualifications.

- Watch for unused credit carryforward options as well as annual claiming limits.

FAQs:

-

- How does the Section 199A pass through deduction compare against the domestic production credit? They stack providing combined benefits for eligible industries.

- What records substantiate R&D tax credit eligibility over time? Lab notebooks, timecards, project cost ledgers, invention disclosures etc.

- Can costs getting expensed under 179 also qualify for R&D credits? Yes, no double dip restrictions exist across those programs.

- What industries qualify for film production write-offs? TV, streaming and live theatrical performances also eligible beyond movies.

- Do inventory accounting rules apply to reseller operations? Yes, COPS exclusions reduce tax liability for wholesale distribution as well.

6. Net Operating Loss (NOL) Carryforwards

-

- Losses Generate NOLs: Annual negative taxable income triggers eligible NOL pool.

- Carry Back and Forward: Apply up to 2 years back getting refunds, or up to 20 years forward.

- Offset Future Tax Liability: Deduct past unutilized losses against income in upcoming profitable years.

- Change Loss Accounting: Temporary rule changes expanded recent NOL benefits.

- Meticulous Recordkeeping: Track NOL origination details for accurate multi-year carry amount monitoring.

Example:

-

- TechStartup Inc lost $500K from 2019 through 2021 as they built products still pre-revenue.

- Once launched in 2022 they showed a $900K profit which the prior losses help offset.

- Meticulous NOL tracking and carryforward documentation supported accurate liability reduction.

- Netting $900K minus up to $500K NOLs claimed provides major tax savings as income scales up.

- Careful accounting and planning enabled them to utilize past losses against future tax bills.

How to Proceed:

-

- Model tax scenarios showing breakeven timing accounting for NOL carryforward deductions.

- Consider filing Form 1139 to expedite losing year refunds from carrybacks.

- Verify state NOL treatment aligns with federal guidance.

- Attach supporting details on returns annually claiming eligible losses against income.

- Monitor expiration windows carefully as 20 year clock ticks on oldest unused amounts.

FAQs:

-

- What forms and schedules report S corp NOL claims on shareholders returns? Reporting happens across Form 1040, Schedule E and carried K-1s.

- Do shareholders need to claim NOLs on pro rata basis aligning with ownership? No special allocations are permitted disproportionately assigning losses.

- Can I choose to forgo carrybacks entirely and just carry losses forward? Yes, this option exists but pursing refunds may provide more immediate liquidity.

- Is gaining IRS pre-approval for NOL deduction plans advisable? Not strictly required but helps prevent future audit challenges.

- What purchase price impacts does extensive NOL carryforwards produce? Significantly higher valuations and goodwill premiums.

7. Vehicle & Equipment Cost Recovery

-

- Bonus Depreciation: Fully deduct 100% of asset costs exceeding annual limits in year placed in service.

- Section 179 Expensing: Elect to deduct up to $1 million in equipment purchases entirely in first year.

- Actual Expense Method: For vehicles, write off portion of annual operating costs like gas, repairs etc.

- Disposition Gains & Losses: Certain tax implications apply when selling previously expensed assets.

- LIFO Inventory Accounting: Matches most recent costs against sales minimizing taxable income.

Example:

-

- XYZ Corp wrote off 100% of their $2 million equipment investment immediately instead of depreciating over 5+ years.

- They tracked vehicle costs directly and could deduct up to $18K under Sec 179 too.

- Combining accelerated depreciation programs provided major tax savings.

- Selling the used assets 5 years later recognized some capital gain income as applicable.

- Proactive offsetting of past depreciation amounts minimized later tax burdens.

How to Proceed:

-

- Run cost-benefit analysis on bonus depreciation vs gradual expensing for expensive purchases.

- Maximize Section 179 treatment for vehicle fleets, heavy equipment etc.

- Consider expected asset holding periods when weighing write-off methods.

- Account for eventual recapture liability accelerating deductions upfront.

- Manage inventory accounting techniques aligning with business volume patterns.

FAQs:

-

- Does the Section 179 deduction limit get adjusted for inflation? Yes, the expense cap increases periodically per IRS rules.

- Can S corps qualify for industry-specific credits like electric vehicle write-offs? Yes, all entities are generally eligible barring restrictions.

- What recapture rate applies on previously expensed assets? Generally matches the bonus depreciation percentages originally claimed.

- Do actual vehicle expense deductions require special mileage logs? Yes, detailed documentation on usage proves business vs personal splits.

- Can passive shareholders also claim asset expense deductions? Rarely, material participation in operations typically must be proven.

8. Qualified Business Income (QBI) Deduction

-

- 20% of Pass-Through Income: Taxpayers can deduct up to 20% of qualified business income from S corps and partnerships.

- Taxable Income Limits: Full write off phases out above $170K individual / $340K joint taxable incomes.

- Qualified Trade or Business: Most exclude law, accounting, health except architects and engineers.

- Aggregation Rules: Smaller entities can group QBI together expanding write offs.

- Stacks Against Other Savings: QBI expands pass through tax benefits even further.

Example:

-

- Susan’s marketing consultant S corp income qualifies for up to the 20% QBI deduction.

- Her taxable income is under the phase out limits to claim the full deduction amount.

- She also aggregates consulting income with her husband’s construction LLC boosting qualified amounts.

- Stacking QBI on other pass through tax savings provides even greater benefit.

- Recently expanded, the QBI deduction targets small businesses exactly like Susan’s.

How to Proceed:

-

- Review eligibility for both entities and trade/business activities.

- Consider grouping related companies under common ownership to maximize amounts.

- Model phase outs under various income scenarios to optimize.

- Combine with other S corp benefits like retirement plan contributions to further minimize taxes.

- Given recent expansion, act fast leveraging the QBI deduction fully before any policy shifts.

FAQs:

-

- What income counts towards the phase out thresholds? Adjusted gross income including all external wages, portfolio incomes etc.

- Can I qualify for QBI in some businesses but not others? Yes, each entity evaluated separately under eligibility rules.

- How is the income phase out calculated for married joint filers? Still applies at $340K unlike some other dual thresholds.

- Do I need to attach any special forms or schedules when claiming QBI? Reporting generally happens directly on personal returns.

- What if my taxable income fluctuates year to year? Plan for variability modeling QBI phase out implications under projections.

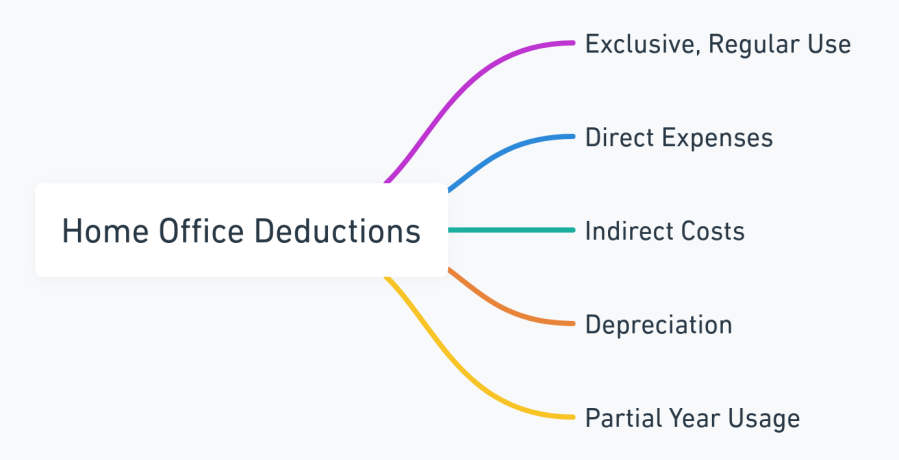

9. Home Office Deductions

-

- Exclusive, Regular Use: Maintain dedicated office space for core admin, management functions.

- Direct Expenses: Deduct rent, repairs, utilities proportionally.

- Indirect Costs: Write off percentages of property taxes and insurance too.

- Depreciation: Claim portion of home value declines over 27.5 year schedule.

- Partial Year Usage: Prorate deductions aligning with days occupied for business needs.

Example:

-

- Jan’s 300 sq ft home office constitutes 18% of personal residence used exclusively as headquarters of her S corp.

- She deducts appropriately allocated shares of monthly rent, electricity and internet expenses from business income taxes.

- When moved in mid-year, calculations prorated write off amounts for length of occupancy.

- Meticulous measurements and usage logs support percentage based deductions from multiple categories.

- Combined direct and indirect fractions of costs provide sizable home office tax savings.

How to Proceed:

-

- Sketch out exact office dimensions and layouts relative to full home blueprints.

- Keep daily logs noting hours occupied for business needs should IRS ever inquire.

- Take photographs documenting work spaces and activities for further validation.

- Actually measure (don’t estimate) square footage percentages allocating costs.

- Consult qualified tax professionals specializing in home based businesses when uncertain.

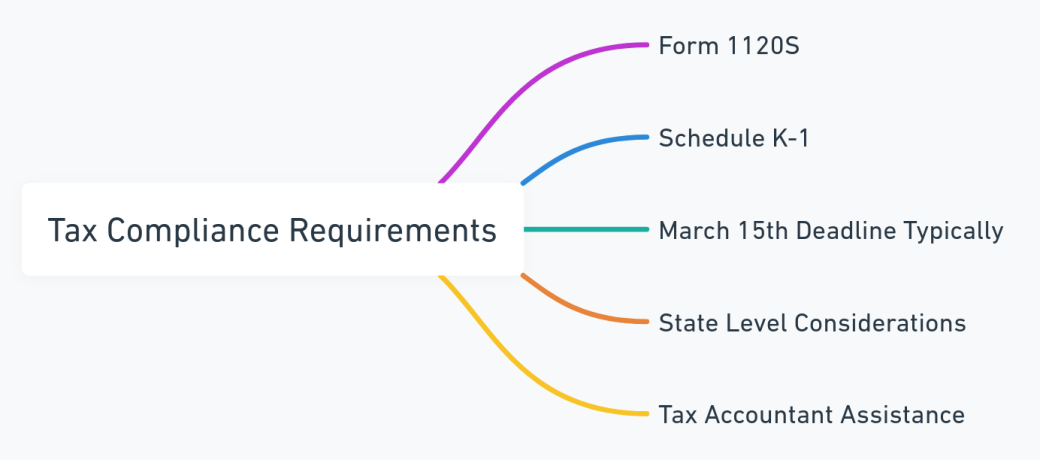

10. Tax Compliance Requirements

-

- Form 1120S: Must file specialized S corp return version annually instead of normal 1120.

- Schedule K-1: Reports all pass-through profit/loss amounts flowing to shareholders.

- March 15th Deadline Typically: Accelerated compared to other entities given pass through treatment.

- State Level Considerations: Some localized taxes still apply for entities to track.

- Tax Accountant Assistance: Given unique treatment, professional support pays dividends.

Example:

-

- Acme LLC successfully filed the necessary Form 2553 to enable specialized S corp taxation last fiscal year.

- Now Accountants R Us will complete the mandatory 1120S with K-1s flowing earned income to owners by March.

- Their CPAs also incorporated state level fees still applicable locally despite federal pass through benefits.

- Careful S corp specific protocols around documentation and deadlines reduced audit risk exposure.

- Relying on tax professionals well versed in all entity election nuances proved essential.

How to Proceed:

-

- Reference IRS resources like S corp guides, forms instructions and common FAQs to stay compliant.

- Ask about any state or local licenses, taxes and registrations needing registration.

- Maintain detailed financial records given lack of corporate taxation requiring reliable support.

- Consider outsourced expert accounting assistance given specialized protocols.

- Note annual deadlines carefully through calendars marking return due dates.

FAQs:

-

- When does my first 1120S need to get filed by after electing S corp status? Tax treatment generally starts the year Form 2553 gets approved even if mid-year.

- What if I discover mistakes on a prior year return – can I amend? Yes, Form 1120X enables corrections though penalties may still apply.

- Do all S corp shareholders need to consent before filing major tax elections? Typically substantial decisions require majority approval.

- Can I switch tax year ends after setting up the S corp? Yes but requires formal approval submitting Form 1128.

- What tax implications arise if S corp status gets revoked accidentally? Immediate C corporation treatment kicks back in with double taxation.

Summary

The intricacies around entity structure selection when launching a business can seem extraordinarily complex for entrepreneurs. However, once deserialized, the mechanics behind critical options like S corporation election unlock major tax advantages.

As highlighted throughout this guide, qualifying private firms can reap benefits like:

- Avoiding C corporation double taxation pitfalls

- Optimizing payroll tax liability

- Expensing operating costs

- Leveraging niche industry credits

- Carrying forward losses

- Accelerating equipment deductions

- Qualifying for QBI write-offs

- Streamlining compliance requirements

In collaborating closely with tax professionals while structuring affairs to extract all available deductions, significant liability savings result. Careful modeling reveals the sizable advantages S corporations thus provide well worth election consideration by ownership groups under the shareholder, income and operational limits permitted.

S Corporation Formation Services

Based on the comprehensive tax benefits outlined in this piece, operating as an S corp likely warrants consideration for your business needs. To expedite smooth company structuring leveraging specialized pass through treatment, our online application kicks off seamless entity election support.

![]()

Our specialized team stays up to date on the latest IRS rules and state specific regulations around S corporations. We file all documentation like Form 2553 while coordinating with accounting and legal partners as needed. Get started today officially classifying your company as an S corp to start reaping tax savings based on our decades of small business advising expertise.

Need Legal Help?

In addition to S corporation election support, our law firm assists small business owners across the full spectrum of operating needs – from daily compliance to intellectual property counseling to HR risk management. Contact us for tailored guidance optimizing legal foundations so you can focus innovation efforts entirely on disrupting markets.

Test Your S Corporation Tax Knowledge

Questions: Payroll & Self-Employment Tax Savings

-

- 1. What minimizes payroll taxes on S-corp income?

- A) High salaries

- B) Low salaries

- C) Bonuses

- D) Distributions

- 2. How can I lower tax bracket exposure?

- A) Retirement plan contributions

- B) Charitable donations

- C) Income splitting

- D) Credits and deductions

- 3. What payroll costs allow expanded deductions?

- A) Office supplies

- B) Health insurance

- C) Commuting costs

- D) 401k contributions

- 4. Can deductions bunch year to year?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 5. Should salary align with qualifications?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 1. What minimizes payroll taxes on S-corp income?

Answers:

-

- 1. B – Paying reasonable salaries based on qualifications allows more income to be distributed as dividends avoiding 15.3% payroll taxes, generating significant savings especially at scale.

- 2. C – Analyzing the tax bracket thresholds and strategically allocating K-1 pass-through income across owners’ individual returns can optimize marginal rates exposure.

- 3. D – Certain qualified retirement plan contributions like 401Ks can expand payroll deductions while also deferring taxes owed by owners.

- 4. A – Given contribution limits, deductions can alternate heavily year to year between profit distributions vs funding pensions for progressive tax minimization over time.

- 5. A -W-2 salary amounts should accurately align with owners’ job qualifications and market rate benchmarks for similar roles to avoid IRS scrutiny.

Questions: General Business Expense Deductions

-

- 1. What home office costs can I deduct?

- A) Rent

- B) Repairs

- C) Utilities

- D) All of the above

- 2. How track vehicle expenses for deductions?

- A) Mileage logs

- B) Actual costs

- C) Both methods

- D) None of the above

- 3. What purchased equipment qualifies for immediate expensing?

- A) Office furniture

- B) Software

- C) Machinery

- D) All of the above

- 4. What principles guide accountable reimbursement plans?

- A) IRS code compliance

- B) Strict policies

- C) Detailed documentation

- D) All of the above

- 5. Why keep meticulous expense records?

- A) Prevent audits

- B) Secure deductions

- C) Maintain compliance

- D) All of the above

- 1. What home office costs can I deduct?

Answers:

-

- 1. D – Prorated shares of rent, utilities, repairs aligning with home office space percentages occupied for admin functions qualify for deductions.

- 2. C – Mileage logs documenting business trips or actual costs like vehicle insurance/fuel can substantiate write-offs claimed.

- 3. D – Section 179 rules enable deducting various equipment like computers, furniture fully in the first year up to specified limits.

- 4. D – Accountable reimbursement plans must comply fully with IRC regulations through strict policy enforcement and diligent documentation.

- 5. D – Meticulous expense documentation prevents audit problems while securing deductions and maintaining compliance.

Questions: Fringe Benefit Tax Write-Offs

-

- 1. What fringe benefits offer deductions?

- A) Group term life insurance

- B) HSAs

- C) Wellness programs

- D) All of the above

- 2. Can I deduct family health insurance costs?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on plan

- 3. Do these require W-2 employee status?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on benefit

- 4. Must offerings align across workers?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on tenure

- 5. Can these benefits boost recruitment/retention too?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on industry

- 1. What fringe benefits offer deductions?

Answers:

-

- 1. D – Premiums towards supplemental life insurance, gym access, health accounts all potentially qualify for deductions.

- 2. A – Health plans can deduct premiums paid covering spouses and tax dependents also under rules.

- 3. A – Typically full-time W-2 status needed for employees to receive these tax-free benefits.

- 4. C – Certain variance permissible based on seniority but rank-and-file should align.

- 5. A – Creative programs boost recruitment, retention, morale significantly.

Questions: Specialized Tax Credits & Deductions

-

- 1. What costs can manufacturers or distributors exclude?

- A) Labor

- B) Raw materials

- C) Inventory

- D) All of the above

- 2. What substantiates R&D tax credit eligibility?

- A) Timesheets

- B) Lab notebooks

- C) Project budgets

- D) All of the above

- 3. What entertainment industry write-offs exist?

- A) Film production

- B) Streaming video

- C) Live theater

- D) All of the above

- 4. Can I qualify credits on expensed equipment?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on equipment

- 5. Do I need pre-approval before claiming deductions?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on deduction

- 1. What costs can manufacturers or distributors exclude?

Answers:

-

- 1. D – Inventory accounting lets manufacturers and resellers exclude all material and production costs before taxable income.

- 2. D – Lab records, project budgets or timecards provide evidentiary support on technical activities required for R&D tax relief.

- 3. D – Film, TV, theatrical shows all allow full expensing of associated production costs in year paid.

- 4. A – No double dip issues arise claiming both equipment-related credits alongside expensing write-offs.

- 5. C – Pre-approval not strictly required but aids certainty around qualification before investing significantly.

Questions: Net Operating Loss (NOL) Carryforwards

-

- 1. What tax documentation reports S corp NOL deductions?

- A) K-1 schedules

- B) 1040 deductions

- C) Form 1040 Schedule E

- D) All of the above

- 2. Can losses get carried back for refunds?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 3. Do losses offset owners’ other income sources?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on sources

- 4. What NOL expiration risks exist?

- A) Carryback windows

- B) Carryforward deadlines

- C) Both expiration types

- D) No expiration deadlines

- 5. How impact company valuations?

- A) Increase substantially

- B) Reduce modestly

- C) No valuation impact

- D) Depends on industry

- 1. What tax documentation reports S corp NOL deductions?

Answers:

-

- 1. D – Shareholder deductions get reported across K-1s, 1040 returns and Schedule E for S corps.

- 2. A – Carrying back up to 2 years allows amending past returns to get refunds on losses.

- 3. A – Deductible against other external wages, investments generating further tax savings.

- 4. B – 20 year carryforward clock risks expiration if unused amounts age out.

- 5. A – Buyers pay substantial premiums for companies with accumulated tax asset NOL pools.

Questions: Equipment & Vehicle Deductions

-

- 1. What enables accelerated depreciation?

- A) Bonus depreciation

- B) Section 179 expensing

- C) Both programs

- D) Neither program

- 2. How track vehicle expense deductions?

- A) Mileage logs

- B) Actual costs

- C) Both methods

- D) Neither method

- 3. What accounting approach matches current costs?

- A) GAAP

- B) LIFO

- C) FIFO

- D) IFRS

- 4. Do industry specific transportation credits apply?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on equipment

- 5. What recapture eventually applies?

- A) Bonus depreciation

- B) Section 179 amounts

- C) Industry credits

- D) Inventory costs

- 1. What enables accelerated depreciation?

Answers:

-

- 1. C – Bonus and Section 179 rules enable fully expensing equipment in year one instead of gradual depreciation.

- 2. C – Mileage logs or actual operating costs method allow vehicle deductions.

- 3. B – LIFO inventory accounting matches most recent material prices to sales minimizing income.

- 4. A – Sector specific transportation electrification credits may provide additional subsidies.

- 5. A – Bonus depreciation percentages originally expensed see future recapture upon asset sales.

Questions: Qualified Business Income (QBI) Deduction

-

- 1. What determines QBI deduction eligibility?

- A) Business activity

- B) Taxable income level

- C) Both criteria

- D) Neither criteria

- 2. How calculated for spouses filing jointly?

- A) $170K threshold

- B) $340K threshold

- C) Doubled phase outs

- D) Stacked separate amounts

- 3. What income sources impact phase outs?

- A) W-2 wages

- B) Investment proceeds

- C) All external income

- D) Foreign business income

- 4. Can I qualify deduction on some entities only?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on ownership

- 5. Does the deduction require special reporting?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on income amount

- 1. What determines QBI deduction eligibility?

Answers:

-

- 1. C – Both trade/business qualification and taxable income threshold determine eligibility.

- 2. B – Still applies at $340K unlike some other dual limits.

- 3. C – All external income sources factor towards phase out calculations.

- 4. A – Determined entity by entity, can qualify on some businesses only.

- 5. B – Goes directly on personal returns without needing specialized filings.

Questions: Home Office Deductions

-

- 1. What home office use requirements exist?

- A) Exclusive use

- B) Regular use

- C) Business functions

- D) All of the above

- 2. Can I deduct indirect costs too?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on costs

- 3. What documentation should I maintain?

- A) Photos

- B) Time logs

- C) Both types

- D) Neither required

- 4. How handle mid-year moves or occupancy changes?

- A) Prorate deductions

- B) Take full year amounts

- C) Eliminate fully

- D) Defer to next year

- 5. Should I consult tax professionals when uncertain?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on deductions

- 1. What home office use requirements exist?

Answers:

-

- 1. D – Exclusive regular administrative use of dedicated home office space allows cost deductions.

- 2. A – Write offs extend to indirect costs like prorated property taxes and home insurance.

- 3. C – Both photos and usage time logs validate office space qualifications if audited.

- 4. A – Prorating write offs aligned with partial year occupancy handles moves/changes.

- 5. A – Those experienced specifically with home based businesses can clarify uncertainty.

Questions: Tax Compliance Requirements

-

- 1. What form must an S corp file annually?

- A) Form 1120

- B) Form 1120S

- C) Form 1040

- D) Form 1065

- 2. How reported on personal tax returns?

- A) K-1 pass through

- B) Special schedules

- C) Supporting statements

- D) Form 1040 only

- 3. What common deadline applies?

- A) January 15

- B) February 15

- C) March 15

- D) April 15

- 4. Do states conform with federal S corp rules?

- A) Yes

- B) No

- C) In certain cases

- D) Depending on state

- 5. Why engage tax professionals?

- A) Expedite filing

- B) Specialized protocols

- C) Both reasons

- D) Neither reason

- 1. What form must an S corp file annually?

Answers:

-

- 1. B – Form 1120S must get filed instead of standard Form 1120 corporate returns.

- 2. A – Via K-1 pass through integrates with owners’ 1040 submission.

- 3. C – March 15th deadline typically applies accelerating timeline.

- 4. C – Some state level taxes still apply beyond federal integration.

- 5. C – Specialized protocols and faster turnaround warrant experienced guidance.

Disclaimer

The tax information presented in this article is intended for general educational purposes only. It should not be construed as specific legal or financial advice tailored for your particular circumstances. We recommend directly consulting licensed tax and legal professionals regarding election of S corporation status and associated tax implications based on nuances unique to your company’s operations, ownership structure, accounting needs and applicable state and federal regulations. Professional guidance can best advise on optimized integration of the tax minimization strategies overviewed here suiting your situation.

Also See

Cybertruck and S Corporations: An Electric Combo for Business Taxes